Danske Q3 2025: Well done for 2025 – Time to attack in 2026?

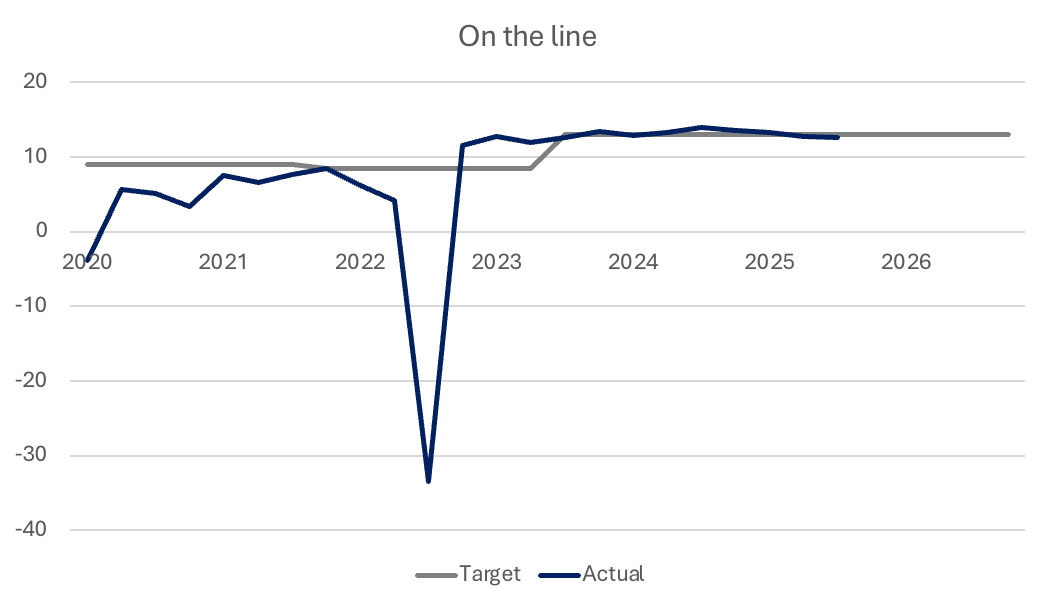

Danske delivered a solid Q3 2025 result today, posting a 12.6% return on equity (ROE). While that’s slightly below the 13% target, it was achieved with a large excess capital buffer tied to temporary regulatory restrictions — ones that will be lifted before year-end.

Since 2023, Danske has consistently hit its financial targets — a welcome turnaround after several difficult years. This improved profitability, however, has been almost entirely driven by higher interest rates: net interest income (NII) contributed 94% of total revenue growth between 2020 and 2024, while all other income lines combined added just 6%.

With rates now falling, top-line pressure will build in 2026 and beyond. Strengthening fee-based income will be essential to ensure sustainable revenue growth going forward.

Danske’s quarterly ROE (%). Source: Danske’s interim reports and factbooks.

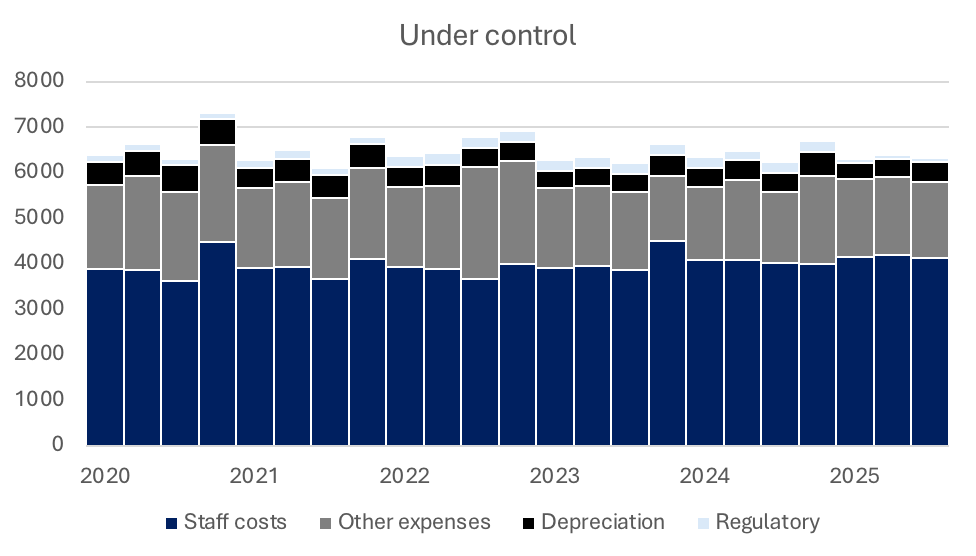

Prudent Cost Management

In one key area, Danske stands out among Nordic peers: cost discipline. The bank has kept operating expenses flat since 2020, avoiding the inflationary drift many competitors are now struggling with.

This gives Danske the flexibility to invest selectively in its strategic growth areas — notably Nordic wholesale banking and retail expansion in Finland and Sweden. So far, management has taken a conservative stance, but 2026 could be the year to step up investment.

Danske’s quarterly expenses (DKKm). Source: Danske’s interim reports and factbooks. Excluding the Estonia AML fine provision in 2022.

Where Will the Capital Go?

Danske’s capital position remains exceptionally strong, with a CET1 ratio of 18.7% — about 2.7 percentage points above its own target and equivalent to DKK 21.5 bn in excess capital.

This provides capacity for substantial M&A activity, should attractive opportunities arise. One area worth strategic attention is asset and wealth management, where Danske’s current footprint (DKK 954 bn in assets under management, AuM) remains only half that of SEB and a quarter of Nordea.

How Do You Like Aktia?

Recent M&A activity has reshaped the Swedish [1] and Danish [2] markets, but Finland has remained quiet since Handelsbanken’s exit. While the Finnish banking and wealth markets are concentrated, several mid-sized players could be viable targets for Danske — notably a few asset managers in the EUR 15–20 bn AuM range, and in banking, Aktia.

Aktia has faced challenges in recent months — multiple CEO changes and ownership shifts — yet it remains a strategically aligned operation. It offers:

A strong wealth management focus, which would strengthen Danske’s positioning in that segment.

A retail footprint concentrated in Finland’s growth regions, matching Danske’s geographical priorities.

A rare opportunity for inorganic growth, as most other Finnish players are non-listed or operate under cooperative structures misaligned with Danske’s corporate model.

Bottom Line

Danske has rebuilt a solid foundation — consistent returns, tight cost control, and one of the strongest capital positions in the Nordics. As regulatory constraints ease and rates normalise, the focus must shift from defence to growth. 2026 could be the year Danske moves from consolidation to controlled expansion, both organically and through selective M&A.

References

[1] https://www.ir.dnb.no/press-and-reports/press-releases/dnb-bank-asa-acquires-carnegie-accelerates-nordic-strategy-and

[2] https://thedigitalbanker.com/three-danish-banks-merge-to-form-al-sydbank/