OP Pohjola Q3 2025: Good Stuff — Too Good?

The OP Financial Group (OP) re-branded itself today to OP Pohjola — and delivered a Q3 2025 result strong enough to make its listed peers wince. The group reported a return on equity (ROE) of 12.2%, not far behind Nordic listed peers. For a cooperative, this is a more-than-solid number, adding further to OP’s already substantial capital buffers, yielding a CET1 ratio of 21%—the region’s highest.

That is bad news for OP’s main competitors, as this financial strength allows them to keep undercutting market pricing on banking and insurance products well into 2026 and beyond.

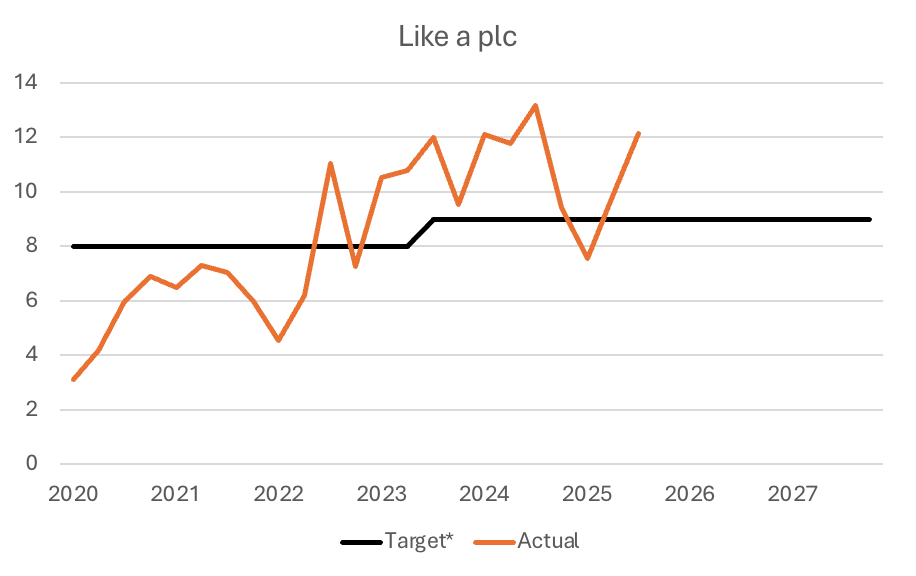

Although OP, as a cooperative, is not run with the sole objective of maximising profit, it does maintain an ROE target — and since 2023, it has been consistently outperforming it.

OP Pohjola’s quarterly ROE (%). Source: OP Pohjola’s interim reports. * Note: OP Pohjola’s official target definition excludes OP bonuses. This author finds such definition economically meaningless, as the bonuses are effectively price discounts and therefore a cost of doing business. The chart tracks actual ROE.

Too Much Money in the Bank?

Since 2020, OP has steadily improved its financial performance, accumulating a capital surplus of +€2.0 billion above its target and +€5.0 billion above regulatory requirements. As the market leader in most retail banking and insurance segments, OP will struggle to deploy this excess capital into business growth without significantly increasing its risk profile.

That begs a clear strategic question: What will OP do with all this money?

One part of the answer came today. OP announced a major increase in its customer bonuses for 2026, expanding their scope and making them more flexible to use. This comes amid increased attention on the bonus system after the government made the bonuses taxable income for recipients, effective 1 January 2026 [1].

OP Pohjola’s annual income, expenses and operating profit (€m). Source: OP Pohjola’s annual reports.

Positive Jaws

Reading OP’s financial statements is not for the faint-hearted. Changes in accounting treatments — notably the adoption of IFRS 17 and the shifting treatment of OP bonuses in the P&L — make long-term comparisons tricky.

Yet, when zooming out, the trend is crystal clear:

Total income grew by more than 50% between 2020 and 2024

Total expenses increased by less than 10% over the same period

Operating profit more than tripled in just four years

This impressive positive operating leverage gives OP a powerful strategic advantage — and a problem most of its competitors would love to have: how to spend all that excess capital without losing its cooperative soul.

Bottom Line

OP Pohjola enters 2026 with capital strength few can match, but capital alone doesn’t win markets. Sustaining a pricing edge through bonuses may work in the short term, but it won’t stop determined competitors from attacking on product, service, and digital experience — areas where listed banks have historically moved faster. The coming years may be less about who has the most money, and more about who uses it best.

References

[1] https://valtioneuvosto.fi/-/10623/hallituksen-esitys-finanssialan-asiakasbonusten-verotuksen-uudistamisesta-lausuntokierrokselle