Handelsbanken Q3 2025: It’s OK — But Is It Enough?

For anyone who has followed the banking sector since the Global Financial Crisis in 2008–2009, the following might sound crazy:

“Consistent 13% return on equity (ROE) is not enough.”

But that’s exactly where we are in the Nordics today — and exactly where Handelsbanken finds itself.

The bank reported a solid Q3 2025 result, with a ROE of 13.3%. In most contexts that would be excellent. But in the current competitive landscape, it’s simply not enough.

Two other large Nordic banks — Nordea and DNB — have both reported a ROE of 15.8% for the same quarter. That is too wide a gap for Handelsbanken to feel good about its relative performance, even if it has no formal ROE target. And this is not a new development.

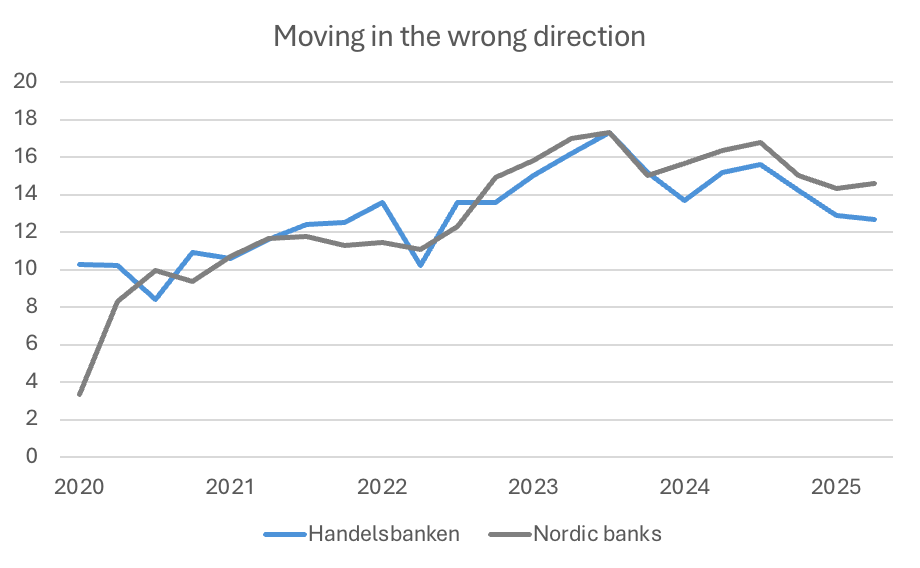

Handelsbanken’s quarterly ROE vs Nordic bank peers including Nordea, Danske, SEB, Swedbank and DNB. Source: Sample banks’ interim reports and factbooks.

Falling Behind the Pack

As the chart above shows, Handelsbanken fell behind its peer group roughly two years ago and hasn’t closed the gap since.

The bank has identified the problem and since early 2024 has taken steps to lower its cost base — and with success. Since Q1 2024, Handelsbanken has decreased staff costs by 7% and other expenses by 25%. This is a strong result and a clear priority for management.

However, revenue has fallen even faster. Handelsbanken is highly dependent on net interest income (NII), which accounts for about 75% of total income. In a declining interest rate environment, this is a structural headwind to its financial performance.

Cost reductions have helped, but they have not been enough to offset the revenue decline. With both income and expenses trending down at a similar pace — and income falling from a higher base — the gap relative to peers has widened.

Handelsbanken’s quarterly total income and total expenses (SEKm). Source: Handelsbanken’s interim reports and factbooks.

Some Bright Spots

Handelsbanken does have a few things going its way. On 30 September 2025, Global Finance named Handelsbanken the safest commercial bank in Europe [1].

Credit quality remains excellent: Q3 2025 marked the seventh consecutive quarter of net credit loss reversals. This is an important strength in an environment where credit quality is becoming a more relevant differentiator again.

Strategic Crossroads

It’s impossible to conclude that Handelsbanken’s Q3 2025 performance was bad — but it clearly lagged its peers. The fact that this has now persisted for two years is concerning.

Even more worrying is that there are no easy answers. Cutting costs is necessary, but it won’t be sufficient on its own. Handelsbanken must find new sources of revenue to close the gap. It has the capital strength to pursue M&A opportunities if they arise. In recent years, however, it has moved in the opposite direction, divesting its Danish and Finnish businesses [2].

The recent sale of Danske Bank’s Norwegian business to Nordea [3] could be seen as a missed opportunity for Handelsbanken to strengthen its position.

Bottom Line

Handelsbanken’s underlying strength remains clear: excellent credit quality, cost discipline, and balance sheet safety. But in today’s market, these are not enough to keep up with peers delivering >15% ROE.

It remains to be seen whether current leadership recognises the full magnitude of the problem — and if they do, whether they can turn it around.

References

[1] https://gfmag.com/award/winner-announcements/press-release-global-finance-names-the-worlds-50-safest-commercial-banks-2025/

[2] https://mb.cision.com/Main/3555/3436107/1483153.pdf

[3] https://www.nordea.com/en/press/2023-07-19/nordea-to-acquire-danske-banks-personal-customer-business-and-associated-savings-assets-in-norway