Nordea Q3 2025: Mission Accomplished for 2025 — Now Comes the Hard Part

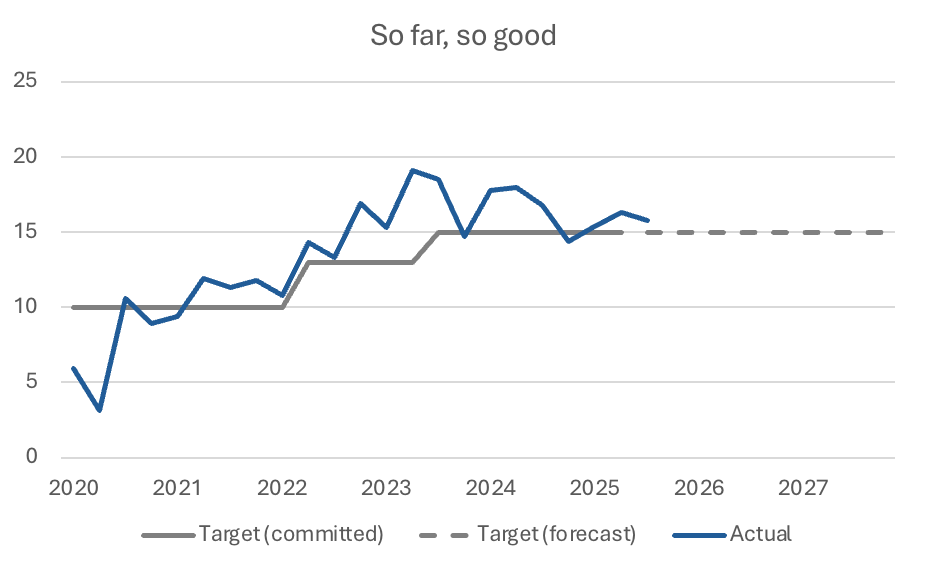

Today, Nordea reported a strong Q3 2025 result, posting a return on equity (ROE) of 15.9%, well above its 15% target. After the first nine months of the year, the ROE stands at 15.8%, meaning Nordea has effectively delivered on its promises to shareholders for the fifth consecutive year. This is an impressive achievement and a clear testament to the current leadership team, which has overseen this sustained period of strong performance.

However, there are two elements that partly cloud Nordea’s underlying performance:

The deposit hedge, and

The management judgement buffer.

Let’s start with the deposit hedge. In Q3 2025, the year-over-year impact of this hedge was €127 million, equivalent to 7% of Nordea’s net interest income (NII) in the quarter. This positive effect will gradually fade as the hedges roll over and assets are repriced. In other words, we won’t have a fully clear picture of Nordea’s underlying NII until late 2026 or 2027.

The second factor is the management judgement buffer. In response to the Covid-19-induced macroeconomic uncertainty, Nordea booked sizeable management overlays, bringing the buffer to €650 million in Q2 2020. This level was maintained well beyond the pandemic, and only recently has the bank started to release it meaningfully—by €60 million and €50 million in the last two quarters, respectively—providing a notable profit boost. With the buffer now approaching its pre-pandemic level, this lever will not be available for much longer, as Nordea expects to release the remainder by end-2026.

Nordea’s quarterly return on equity (%). Source: Nordea interim reports and factbooks.

This brings us to Nordea’s outlook for 2026 and beyond. I will take a deeper look at this topic after Nordea’s Capital Markets Day on 5 November 2025, but even at this stage it’s clear that reaching the next ROE target will be challenging. I expect Nordea to maintain its current ROE target of 15% in the upcoming strategy period, but delivering on that ambition will require significant effort.

As noted earlier, the NII headwind will intensify in 2026 and beyond. In addition, another pressure point seems to be emerging on the cost side.

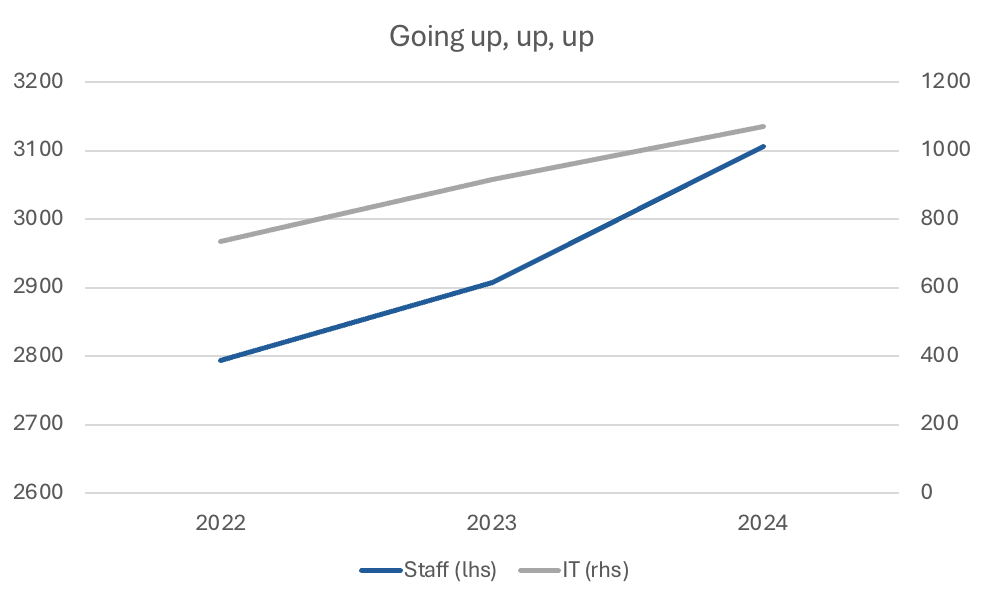

While Nordea’s total costs remained broadly stable in Q3 2025, there are two cost categories worth watching closely going forward: staff costs and IT expenses.

Nordea’s annual staff and IT expenses, before capitalisation (€m). Source: Nordea annual reports.

Both staff and IT expenses (before capitalisation) at Nordea increased by more than €300 million between 2022 and 2024, representing close to 20% growth. A large share of the IT costs has been capitalised, and is therefore not immediately visible in the income statement (and not reported in full detail in the interim reports).

This cost increase is largely linked to Nordea’s strategic investments in technology and risk management, which the bank has stated will be wound down in the coming quarters. If this materialises, the cost pressure may ease and not pose a major issue. However, if these investments have pushed the underlying cost base to a structurally higher level, Nordea will face a significant headwind heading into 2026.

In summary, Nordea has delivered a strong Q3 2025 and is comfortably on track to exceed its full-year profitability target. But as outlined above, there are both revenue and cost headwinds that need to be managed carefully to extend the five-year track record of meeting and exceeding investor expectations.

Given that the current leadership has never missed its target, all of this sets the stage for an extremely interesting Capital Markets Day in November.