Swedbank Q3 2025: Going Strong — But Work Still to Be Done

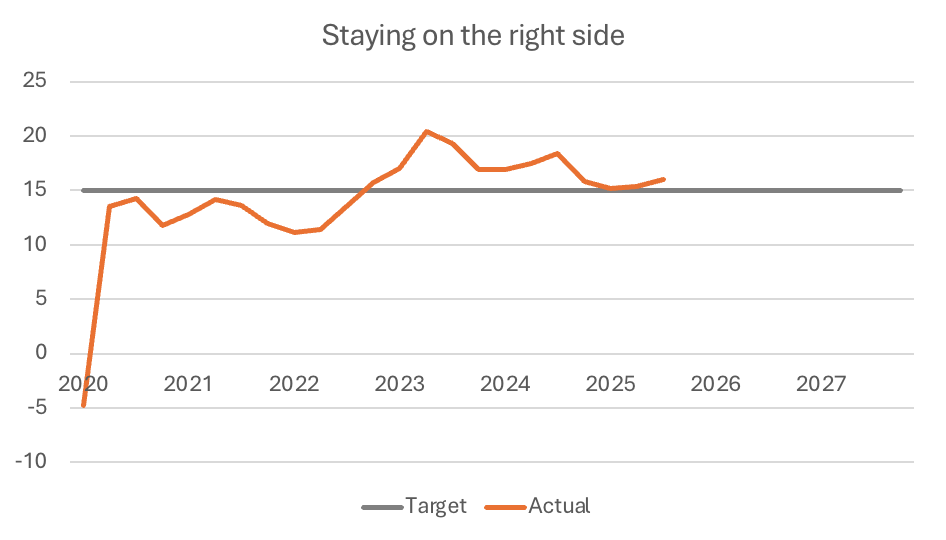

Swedbank reported a strong Q3 2025 result today, delivering a market-leading return on equity (ROE) of 16%. This is an excellent performance and brings Swedbank’s year-to-date ROE to 15.4%, just above their 15% target.

The bank heads into the final months of the year in a strong position, but it can’t afford to take its foot off the gas. Continued discipline will be required to ensure they meet their full-year target for a third consecutive year.

Swedbank’s quarterly return on equity (%). Source: Swedbank’s interim reports and factbooks.

Solid Momentum, but Risks Are There

But Swedbank is not immune to changing market conditions and faces the same challenges as its competitors. Two stand out in particular:

Heavy reliance on net interest income — around two-thirds of Swedbank’s total revenues come from this source, which faces headwinds in a falling interest rate environment.

Rising expense levels, which could challenge profitability if income growth slows.

That said, Swedbank has so far managed this balance exceptionally well. Since Q1 2022, expenses have risen by 24%, while revenues have increased by more than 50%. This has resulted in a remarkable 88% increase in operating profit, an exceptionally strong positive operating leverage.

A Powerful Capital Position

A particularly interesting aspect of Swedbank’s current position is its excess capital. The bank holds around 4.8% in total excess CET1, equivalent to more than SEK 40 billion, of which SEK 17 bn is above their own target level. For context, DNB’s recent acquisition of Carnegie cost roughly SEK 12 billion [1]. This means Swedbank is well positioned to make major strategic moves if it chooses to.

For now, the bank is holding back due to the ongoing U.S. investigations, but once these are resolved — and assuming no material penalties — Swedbank could either go on the offensive through acquisitions or reward shareholders with a significant extra dividend.

Bottom Line

Swedbank stands in a very strong position, with market-leading profitability and a powerful capital base. But maintaining this lead will require tight cost control and a clear strategic direction in a changing rate environment.

References

[1] https://www.ir.dnb.no/press-and-reports/press-releases/dnb-bank-asa-acquires-carnegie-accelerates-nordic-strategy-and