The Efficiency Wall in Nordic Banking

Why flat costs won’t be enough in 2026 — and what the banks must do next

As I wrote in my most recent Nordic Banking Insights analysis, while still highly profitable and globally efficient, the large Nordic banks are entering a new phase of structural pressure. Cost levels have risen sharply since 2020, and the tailwind from higher interest rates is now fading in most markets. To understand how serious this cost challenge has become — and what it means for competitiveness in 2026 and beyond — in this article I take a deeper look at the cost and income dynamics of the major Nordic banks. I also outline what the next generation of cost transformation will require.

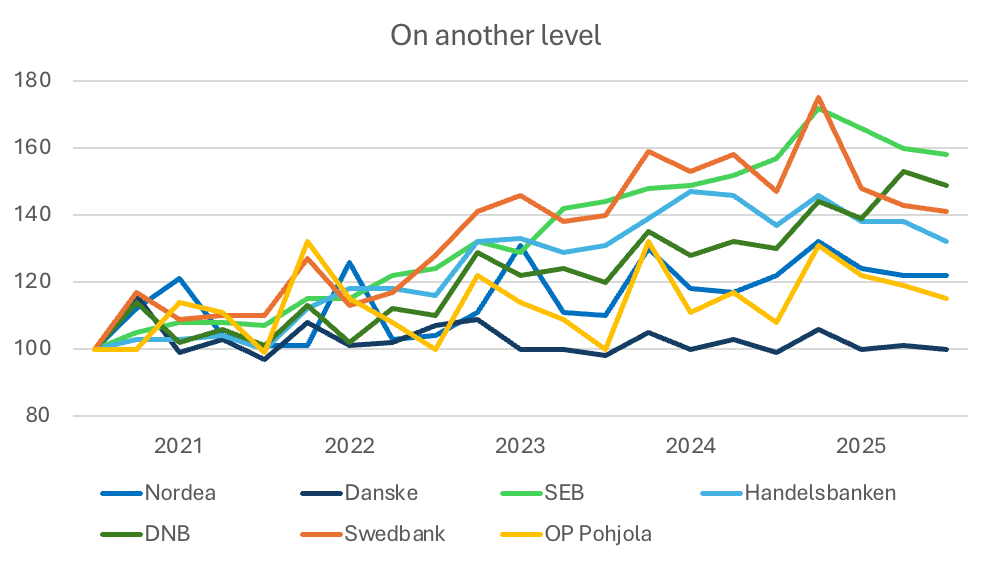

Chart 1: Banks’ quarterly expenses, incl. regulatory levies, excluding administrative fines, Q3 2020 – Q3 2025, rebased = 100. Source: banks’ interim reports and factbooks.

A New Baseline

As Chart 1 illustrates, the Nordic banks are now operating at an entirely new cost level compared to the pre-rate-hike years. Between Q3 2020 and the 2024 peak, most banks saw nominal expenses rise by 25–80%, driven by wage pressure in tech, data and risk; an expanding regulatory agenda across AML, sanctions, operational resilience and ESG; significant ongoing technology modernisation programmes; and, especially in the case of SEB, OP and DNB, multi-year strategic investments and capability build.

Most banks reached their cost peak in late 2024 and have since been able to flatten or even reduce costs modestly. This pattern is visible across all banks, with the sole exception being DNB, whose higher cost base is primarily the result of strategic M&A — most notably the Carnegie acquisition — which has also lifted revenue and diversified the business.

But the fundamental point remains: A new baseline has been set.

Many banks are now running 20–50% above their 2020 cost levels, even after the recent pullback.

This is the root of the efficiency challenge.

Why this matters: revenue has already turned

Cost increases are manageable when revenue grows at equal or faster pace. And indeed, 2022–2024 were exceptional years for the Nordic banks. A once-in-a-generation net interest income (NII) surge lifted income, profitability and returns.

That chapter is now closing.

With policy rates expected to remain stable — or decline — through 2026–27, revenue momentum is normalising. Loan demand remains modest, deposit spreads have compressed, and fee income, while stable, is not strong enough to offset the gradual decline in NII.

This is why the next lens is critical: the cost-to-income ratio.

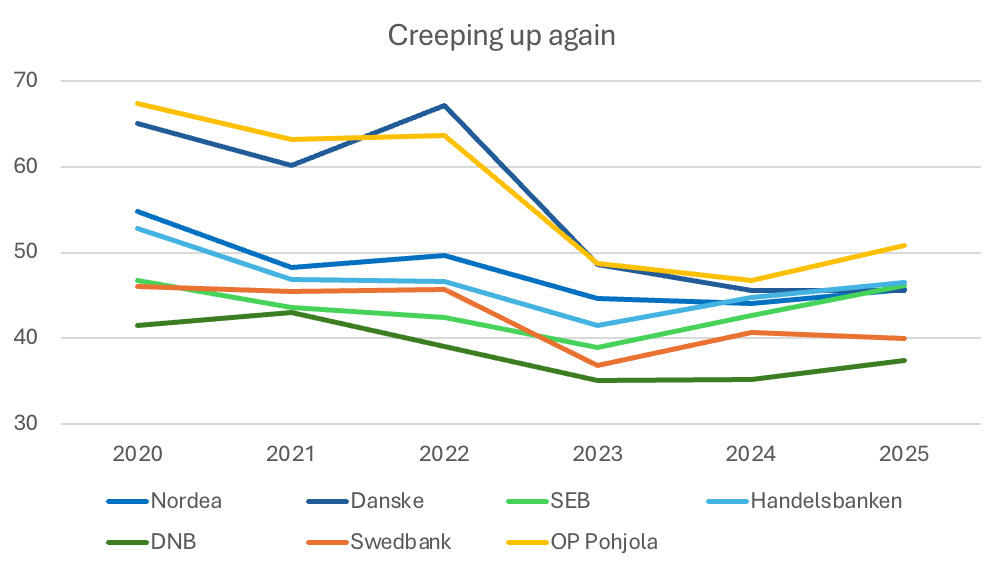

Chart 2: Banks’ annual cost-to-income (C/I) ratio (%), incl. regulatory levies, excluding administrative fines, 2020 – 9M 2025, rebased = 100. Source: banks’ annual and Q3 2025 interim reports.

C/I ratios are turning again

As Chart 2 shows, most banks saw their C/I ratios bottom out in 2023–24 and begin to rise again during 2025. This convergence tells a clear and consistent story:

the revenue plateau has already arrived,

the cost base sits at a materially higher structural level,

and the efficiency gains of 2022–24 were cyclical, not structural.

If banks take no further action, cost-to-income ratios are likely to trend upward through 2026–27, even in the absence of further cost increases.

This is the essence of the efficiency wall.

Short-term fixes are not enough

To date, the industry response has been dominated by tactical, short-lived measures.

Recruitment freezes — used by Nordea, SEB and Swedbank — provide immediate relief but do not touch the deeper sources of cost inflation: fragmented operating models, overlapping organisational layers, and a workforce mix heavily weighted toward highly specialised expert functions. Once investment cycles resume, cost drift naturally returns.

Some banks have also opted to shrink their business. Danske and Handelsbanken have taken steps to refocus, reduce geographic presence, or simplify product sets. While this helps costs, it invariably pressures revenue and limits future growth in fee and lending income. Neither bank has fully solved that trade-off.

These levers buy time. They do not resolve the structural gap between the new cost baseline and normalised income.

What the data really shows

Looking beyond short-term fluctuations, the combination of cost trajectory, income momentum and strategic positioning places the banks into three distinct categories.

1. On top of the wall: DNB and Swedbank

These banks continue to operate with world-class C/I ratios in the <40s, despite the inflationary cycle.

DNB has a higher cost base today than in 2020, but this is almost entirely the result of strategic M&A and business expansion. Its efficiency remains the best in the region. Cost growth has been more than offset by revenue expansion, and the balance between spending, income and diversification remains healthy.

Swedbank benefits from a simpler operating model and strong cost discipline. Its costs peaked in 2024 but have since declined meaningfully. The bank has demonstrated consistent jaws management, and as result has delivered the best profitability among the peer group in recent years.

These banks are not struggling with cost control. Their challenge is maintaining this position as income normalises.

2. Managing the wall: Nordea, Danske and OP Pohjola — and yes, Handelsbanken

These banks have handled cost pressures relatively well, but now face a structural test.

Nordea has kept its cost line flatter than most of its peers and has reduced its expenses in recent quarters. Its next efficiency gains will come from large-scale platform consolidation, Nordic shared capabilities and broad AI deployment. The key question is whether these levers can offset the expected NII pressure in 2026 and, ultimately, enable Nordea to deliver on its highly ambitious 40–42% C/I target for 2030.

Danske is the only bank whose nominal cost base is roughly unchanged from 2020. With the AML remediation cycle now behind it, and a more focused business model, Danske is well positioned — but still dependent on revenue growth or pricing power to keep efficiency from slipping.

OP Pohjola, despite a high structural cost burden from ICT and compliance, has managed its cost development far better than the topline numbers suggest. Its expense trajectory has broadly mirrored its peers’ downward trend in recent quarters. For a cooperative with no external shareholder pressure, a C/I above 50% is not comfortable — but not alarming either. OP’s biggest challenge is not imminent cost distress, but the long-term question of how to convert its sizeable investments into productivity and process simplification.

Handelsbanken is a special case. Its costs have come down from their 2024 peak, and the bank has taken meaningful steps to simplify its footprint and reduce central overhead. However, this moderation in expenses has been accompanied by a steady decline in revenue and falling ROE, among the lowest in the Nordic peer group. Handelsbanken is therefore not “on top of the wall” nor in acute cost difficulty; instead, it is managing the wall from a weaker strategic position. The bank is efficient operationally, but its efficiency is increasingly constrained by a shrinking business model, limited fee growth and reduced scale advantages. The key question for Handelsbanken is no longer cost control alone, but whether it can reignite revenue momentum while keeping its simplified operating model intact.

These three banks are not in immediate difficulty. But they are entering the phase where flat costs will no longer be enough.

3. Pushing into the wall: SEB

SEB remains the most pronounced example of the efficiency wall in action.

The bank has seen the strongest cumulative cost inflation of the group — between +50–60% from the 2020 baseline — driven by cloud modernisation, platform investments, AI, embedded finance initiatives, and risk and compliance strengthening.

Costs have begun to fall from their 2024 peak, but they remain far above previous levels. As revenue normalises, SEB faces the clearest dependency on its transformation agenda: the savings must become tangible, and quickly.

SEB is not in trouble. But it is the bank most exposed to the transition from investment-driven growth to efficiency-driven performance.

What must happen next

Breaking through the efficiency wall requires a shift from tactical cost controls to deep operating-model redesign. The next decade’s winners will be those that reduce structural complexity, accelerate decision cycles, and embed productivity into the very fabric of their organisation.

End-to-end value stream organisation

The first step is to abandon the traditional structure of separate business areas, technology units and operations functions. Nordic banks have talked for years about end-to-end processes — mortgages, payments, onboarding, SME lending — but these efforts rarely translate into organising around those processes. In a modern, fast-moving banking environment, no end-to-end process can be truly efficient if one executive owns the customer relationship, another owns the technology, and a third owns the operational steps in between. A handful of banks, most notably OP Pohjola, have gone further than their peers in deploying agile operating models at scale. But even in OP’s case, strategic ownership, budgeting authority and people leadership remain anchored in traditional business and IT organisations. True simplification begins only when end-to-end ownership and accountability mirror the actual customer journey, rather than the legacy organisational chart.

Skill-based workforce

A redesigned organisation requires a redesigned workforce. This means shifting from rigid functional silos to skills-based pools, capability hubs and cross-country delivery teams. Contrary to common misconception, agile operating models do not remove structure or discipline — they increase it. Teams must operate within strict guardrails, follow shared standards, and take full accountability for their delivery. This approach is demanding, but it is the only way to achieve the speed and productivity required to compete under a higher cost baseline.

Automation and AI

The next lever is automation and AI — not in the limited, pilot-driven form many banks have adopted, but in broad deployment across the highest-volume, highest-cost domains. Nowhere is the opportunity greater than in financial crime operations. Thousands of employees across the Nordic banks perform largely manual KYC, transaction monitoring and sanctions screening tasks. The technology exists to automate much of this work, but fear-based decision-making and regulatory caution have held progress back. A few banks have begun modernising credit administration, onboarding and product management workflows; in 2026, these will need to move from experiments to large-scale implementation.

Shared platforms

Technology consolidation is the next frontier. Nordic banks still operate on fragmented system landscapes, especially those with multi-country footprints. New core platforms, shared payments systems, cloud adoption and third-party utilities have moved the region forward, but not far enough. Real transformation requires application reduction, shared architectures and common platforms — changes that are only possible once the process, workforce and automation foundations are in place.

Transparent pricing

Finally, pricing and monetisation discipline must evolve. Efficiency is ultimately about the balance between costs and income, and under a structurally higher cost base, banks cannot rely solely on expense measures to preserve competitiveness. As income normalises, the ability to price essential services — advice, payments, wealth, and bundled offerings — in a way that reflects their true value becomes part of the overall efficiency equation. Nordic banks have historically under-priced or cross-subsidised many of these services, a model that worked during periods of elevated NII but is no longer sustainable under the new baseline.

Bottom Line

The Nordic banking model has been the global benchmark for efficiency for years. But the next cycle will look different. Revenues are normalising. The cost base has reset. The easy efficiency wins are behind us.

The question is no longer whether banks can freeze hiring or trim costs at the margin. They can, and many have. The real question is whether they can redesign their operating models to break through the efficiency wall.

Those who do will set the next global standard.

Those who don’t will watch their C/I ratios drift upward, year after year.

Sources and Methodology

This analysis is based on publicly available financial and strategic disclosures from the Nordic banks, including their 2020–2025 interim reports, annual reports, factbooks and CMD/Investor Presentation materials. Cost and C/I trajectories are derived from reported figures, adjusted for administrative fines and rebased for comparability. Strategic references to DNB’s acquisition of Carnegie, Danske’s portfolio optimisation and Handelsbanken’s footprint adjustments are drawn from the respective transaction announcements and investor materials.